Zero-Cost Collars: Are They Really Free?

Zero-cost collars limit downside without upfront premiums but cap upside and carry hidden opportunity, liquidity, tax, and assignment costs.

Zero-cost collars offer a way to protect investments without upfront costs by balancing the premiums of a protective put and a covered call. While they provide downside protection, the trade-off is capped upside potential. This strategy suits investors looking for cost-conscious risk management over short periods but comes with opportunity costs and limitations.

Key Points:

- Zero-cost collars: Protect against losses but cap gains above the call strike.

- Non-zero-cost collars: Allow more customization but require upfront costs.

- Protective puts: Offer unlimited upside but involve annual premiums.

- Covered calls: Generate income but provide minimal downside protection.

- Unhedged stock: Maximizes growth but leaves you fully exposed to losses.

Quick Comparison:

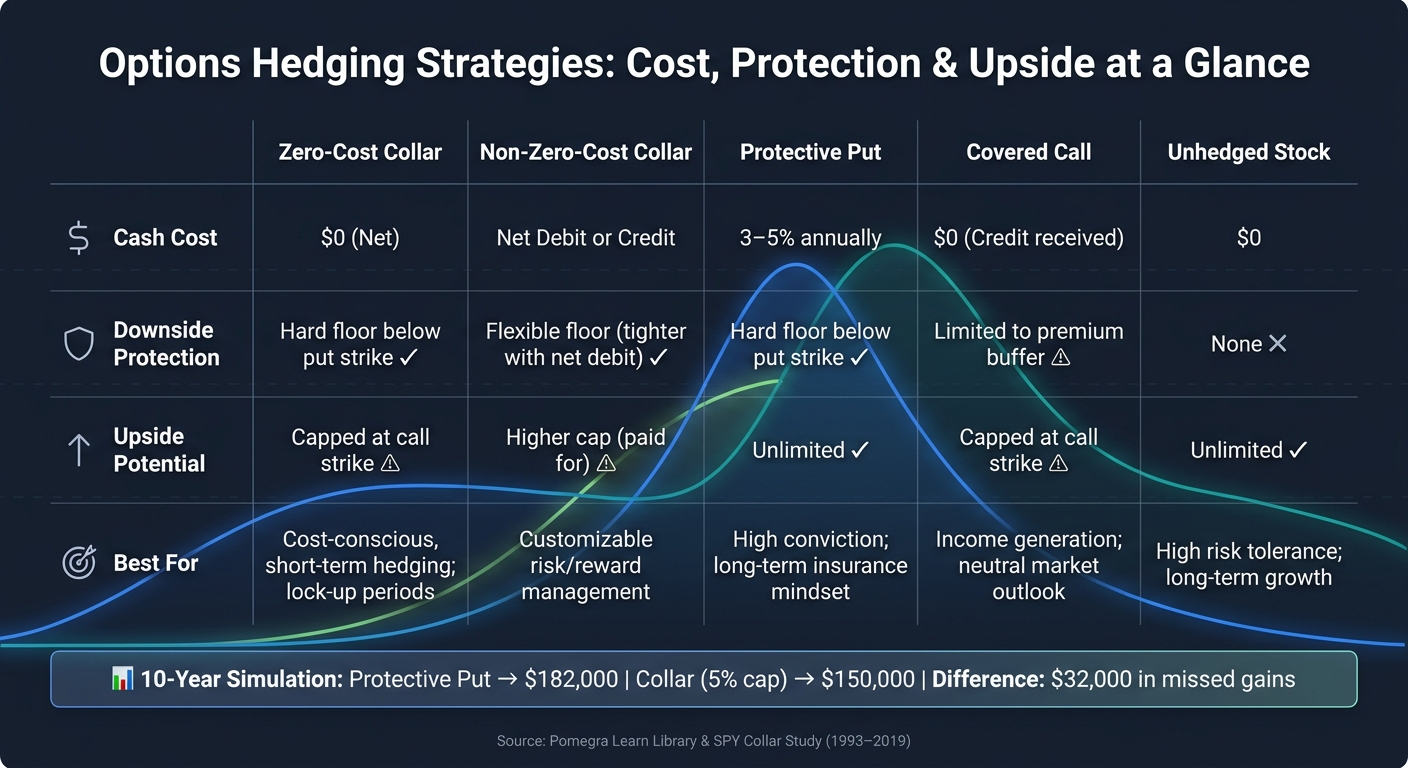

| Strategy | Cash Cost | Downside Protection | Upside Potential | Best For |

|---|---|---|---|---|

| Zero-Cost Collar | $0 (Net) | Hard floor below put strike | Capped at call strike | Cost-conscious, short-term hedging |

| Non-Zero-Cost Collar | Net debit/credit | Flexible floor | Higher cap (paid for) | Customizable risk/reward management |

| Protective Put | Premium (3–5%) | Hard floor below put strike | Unlimited | High conviction, long-term insurance |

| Covered Call | $0 (Credit) | Limited to premium buffer | Capped at call strike | Income generation, neutral outlook |

| Unhedged Stock | $0 | None | Unlimited | High risk tolerance, long-term growth |

Zero-cost collars aren’t entirely “free” due to capped gains and indirect costs like opportunity loss. They work best for specific, short-term needs, but understanding the trade-offs is crucial before choosing this or any other strategy.

Options Hedging Strategies Compared: Cost, Protection & Upside

1. Zero-Cost Collars

A zero-cost collar is a strategy that combines three elements: stock ownership, a purchased protective put (your downside floor), and a sold covered call (your upside ceiling). The premium earned from selling the call offsets the cost of buying the put, which is why it's referred to as "zero-cost" in terms of option premiums.

Upfront Costs

While the options themselves may balance out in cost, there are still transaction-related expenses. Brokerage fees and bid-ask spreads can add up, especially for stocks that aren't heavily traded. For mid-cap or less liquid stocks, these spreads might range between 1% and 2% of the position's value. Additionally, due to the way options are priced - known as put skew - the call strike often needs to be closer to the current stock price than the put strike to achieve a zero-cost structure.

Upside Potential

This strategy limits your ability to benefit from significant price increases. If the stock price rises beyond your call strike, any further gains are forfeited to the call buyer. For instance, if a stock is trading at $100, you might set up a collar by purchasing a $90 put and selling a $110 call. If the stock jumps to $130, your gains are capped at $110 because the call you sold gets exercised.

Downside Protection

On the flip side, the protective put provides a safety net. Using the same $100 stock example, your maximum loss is restricted to the $10 difference between the stock price and the $90 put strike, no matter how far the stock drops. Within the $90 to $110 range, your position functions like owning the stock outright, where gains and losses move dollar-for-dollar with the stock price.

Opportunity Costs

This strategy inherently involves trading off potential profits for downside protection. A study of the SPDR S&P 500 ETF (SPY) from January 1993 to March 2019 examined a zero-cost collar with a 10% floor and a 5% cap. It found that the call was exercised in 55% of six-month rolling periods, resulting in an average of 7.3% in missed gains each time. Conversely, the protective put was triggered in only 7.1% of those periods. This means that while the collar provides peace of mind, the downside protection is rarely needed, and the opportunity cost of capping gains can be substantial.

"A collar explicitly says: I will accept a maximum gain of X in exchange for a maximum loss of Y." - Ernie, Author at FOTW

| Input | Action | Trade-off |

|---|---|---|

| Floor (Put Strike) | Raise closer to the stock price | Increases the cost of the put; requires lowering the call strike to maintain zero cost |

| Cap (Call Strike) | Raise for greater upside potential | Increases the likelihood of the call being exercised, further limiting gains |

| Expiration | Lengthen the timeframe | Increases premiums for both options and locks you into the strategy longer |

Next, we'll explore how non-zero-cost collars compare to this approach.

sbb-itb-a9ac3c2

2. Non-Zero-Cost Collars

A non-zero-cost collar shares the same basic structure as its zero-cost counterpart: you hold the stock, buy a protective put, and sell a call. However, in this version, the premiums don't offset each other entirely. Depending on how the strikes are set, you might pay an upfront net debit or receive a net credit.

Upfront Costs

A net debit happens when you prioritize stronger downside protection, such as setting the put strike closer to the stock's current price. On the flip side, a net credit arises when the call premium exceeds the cost of the put. This typically means accepting a much lower cap on potential gains. For instance, insuring a $400,000 mid-cap tech stock with a 1-year protective put offering a 30% floor could cost between $12,500 and $20,000 in premiums.

Upside Potential

The trade-off becomes clear when considering the strategy's impact on future gains. Investors often choose to pay a net debit to set the call strike further out-of-the-money, allowing for greater upside. In a zero-cost collar, the call strike is dictated by market conditions to offset the put's cost. With a non-zero-cost collar, you’re essentially paying extra to raise the cap. The logic is simple: the more you spend upfront, the higher the potential ceiling for gains.

Downside Protection

The protective floor functions the same way as it does in a zero-cost collar, limiting losses to the gap between the stock price and the put strike. However, unlike a zero-cost collar, which often requires a 10–15% gap between the stock and the put strike, a net-debit collar offers more flexibility. It allows you to set a tighter floor, closer to the stock's current price, providing more precise protection.

Opportunity Costs

Even with a higher cap on gains, the strategy still imposes limits. Over a 10-year period, a stock growing at 7% annually would result in a net wealth of $182,000 on a $100,000 initial position if protected with a put strategy (costing 15% in total premiums). In contrast, a collar capped at 5% annual upside would only grow to $150,000 - leaving a $32,000 difference to the put's advantage. While non-zero-cost collars offer customization, the higher upfront costs and long-term growth restrictions remain key considerations.

| Feature | Zero-Cost Collar | Non-Zero-Cost (Net Debit) Collar |

|---|---|---|

| Upfront Cash Outlay | $0 | Net debit incurred |

| Upside Cap | Lower (set by market conditions) | Higher (bought with net premium) |

| Downside Floor | Wider gap from current price | Can be tighter to current price |

| Primary Use Case | Cost-neutral risk management | Customizable risk/reward profile |

For investors needing to model these trade-offs, AI-powered portfolio analysis can simulate how different collar strikes affect long-term returns.

This setup contrasts sharply with dedicated protective put strategies, which will be analyzed further, or you can analyze your portfolio's risk to see how these strategies impact your specific holdings.

3. Protective Puts

Protective puts offer a way to safeguard your investments by capping downside risk while keeping your upside potential unlimited. The concept is straightforward: you own a stock and purchase a put option. This option gives you the right to sell the stock at a predetermined price - your "floor" - regardless of how much the stock drops. Think of it as insurance for your portfolio: you pay a premium upfront to ensure protection against significant losses.

Upfront Costs

Unlike a collar strategy, protective puts require an upfront payment with no offsetting income from selling a call. The cost is the full premium, typically ranging between 3% and 5% of the position's value annually. For example, a 1-year protective put on a $400,000 position in NVIDIA (NVDA) with a 30% floor was priced at around $18,650 - about 4.7% of the position’s value. This expense is incurred before any market movement, making it a notable initial outlay.

Upside Potential

One of the standout features of protective puts is that they leave your upside fully intact. Since you're not selling a call, there's no cap on your gains. If the stock price doubles, you benefit from the entire increase minus the cost of the premium. This makes protective puts particularly appealing to investors who believe strongly in the long-term growth of their stock but still want to mitigate potential losses.

Downside Protection

The "floor" established by the put strike ensures that if the stock price drops below this level, the rising value of the put offsets the loss. However, it’s worth noting that implied volatility can drive up premium costs, especially during times of market stress when protection is most needed.

Opportunity Costs

The cost of the premium can add up over time, creating a drag on returns. For instance, paying a 3% annual premium results in a cumulative cost of about 26% of the position's value over 10 years, assuming the stock price remains flat. Even in growth scenarios, the ongoing premium reduces net returns compared to an unhedged position. Essentially, the premium is the price you pay for peace of mind.

| Feature | Protective Put |

|---|---|

| Upfront Cash Cost | Full premium (typically 3–5% annually) |

| Upside Potential | Unlimited (minus premium paid) |

| Downside Protection | Hard floor at the put strike |

| IV Exposure | Fully exposed to implied volatility spikes |

| Primary Cost Type | Explicit cash outlay |

4. Covered Calls

A covered call is one of the simpler ways to generate income using options. Here’s how it works: you own shares of a stock and sell someone the right to buy those shares at a set price (the strike price) by a specific date. In exchange, you get a premium, which is credited to your account as soon as the trade is completed.

Upfront Cash Flow

The beauty of covered calls is that you collect cash immediately. For example, selling a call on a stock trading at $100 might bring in $2.50 per share. That premium is yours to keep, no matter what happens next.

Upside Limits

While this strategy provides income, it comes with a trade-off: your profit is capped at the strike price. If the stock jumps from $100 to $140 and your strike is $110, you only gain $10 per share. Any additional upside goes to the call buyer.

Limited Downside Protection

Covered calls offer a small cushion against losses, but it’s limited to the premium you collect. If the stock drops significantly, the premium won’t offset the full decline in value.

The Opportunity Cost Factor

One of the biggest considerations is the opportunity cost. By capping your upside, you may miss out on significant gains if the stock performs exceptionally well. This makes covered calls more suitable for those with a neutral or slightly bullish outlook who are more focused on generating consistent income rather than chasing large price increases.

| Feature | Covered Call |

|---|---|

| Upfront Cash Flow | Positive (premium collected) |

| Downside Protection | Limited (premium acts as a buffer) |

| Upside Potential | Capped at the strike price |

| Primary Cost Type | Opportunity cost (missed upside) |

| Best Suited For | Income generation, neutral outlook |

In the next section, we’ll look at how unhedged stock performs to better understand the trade-offs involved in this strategy.

5. Unhedged Stock

Unlike hedged strategies that use protective measures to manage risk, holding unhedged stock involves fully embracing market movements. This approach means owning shares outright, riding the ups and downs of the market, and avoiding additional costs associated with hedging.

Upfront Costs

When you hold unhedged stock, there are no extra costs beyond the purchase price of the shares. In contrast, a protective put - a common hedging tool - typically costs between 3% and 5% of your position's value per year. Over a decade with a flat stock price, this could add up to about 26% of the position's total value in expenses.

Upside Potential

Unhedged stock moves dollar-for-dollar with the underlying share price, offering unlimited upside potential. If the stock doubles, you capture every dollar of that increase. There are no call strikes limiting your gains or premiums eating into your returns. This makes unhedged stock appealing to investors with strong confidence in a near-term price surge. However, this full exposure to upside also means bearing the full brunt of any downside.

Downside Protection and Opportunity Costs

The biggest vulnerability of unhedged stock is the lack of a safety net. For example, if a stock drops from $100 to $50, a 1,000-share position would lose $50,000 outright. By comparison, a zero-cost collar with a $90 put floor could limit that loss to around $10,000. Every dollar the stock loses directly reduces your investment. Beyond the immediate financial hit, a large drop in value also reduces the capital you have available for recovery or reinvestment - an opportunity cost that can grow over time. While hedged strategies come with their own expenses, such as premiums or capped gains, unhedged stock leaves you fully exposed, with no built-in mechanism to limit losses.

| Feature | Unhedged Stock |

|---|---|

| Upfront Cash Cost | $0 |

| Downside Protection | None – the position has no floor |

| Upside Potential | Unlimited (tracks stock price 1:1) |

| Primary Cost Type | Potential capital loss during downturns |

| Best Suited For | High-conviction investors who can tolerate volatility |

These factors highlight the risks and rewards of holding unhedged stock, setting the stage for a deeper comparison of various strategies.

Pros and Cons

Let’s break down the strengths and weaknesses of each strategy to help you align them with your investment goals.

Zero-cost collars offer a way to protect your downside without an upfront cash expense. However, they come with a trade-off: any gains beyond the call strike are off the table. These are particularly helpful for situations like concentrated positions, executive lock-ups, or when selling isn’t feasible. But in a strong bull market, the capped upside can feel restrictive.

Protective puts provide unlimited upside potential while securing a hard floor against losses, but they come at the cost of an annual premium. This makes them more appealing to investors who have strong confidence in their positions and view the premium as a form of "insurance" against significant declines.

Covered calls generate monthly income with covered calls, but the downside protection is minimal - limited to the premium earned. These work best in flat or slightly bullish markets, where the income can offset minor losses, but they leave you vulnerable to steep price drops.

Finally, unhedged stock is the most straightforward and aggressive approach. There’s no cost, no cap on gains, but also no safety net. This strategy is ideal for those with a high tolerance for risk and a focus on long-term growth.

| Strategy | Cash Cost | Downside Protection | Upside Potential | Best For |

|---|---|---|---|---|

| Zero-Cost Collar | $0 (Net) | Hard floor below put strike | Capped at call strike | Cash-constrained hedging; lock-up periods |

| Protective Put | Explicit annual premium | Hard floor below put strike | Unlimited | High conviction; "insurance" mindset |

| Covered Call | $0 (Credit received) | Limited to the premium buffer | Capped at call strike | Income generation; neutral outlook |

| Unhedged Stock | $0 | None - full exposure | Unlimited | Maximum long-term growth; high risk tolerance |

It’s important to note that collars are tactical tools, not long-term fixes. For example, a 10-year simulation assuming 7% annual returns revealed that a protective put strategy generated $182,000 in net wealth, while a collar strategy capped at 5% annual upside produced $150,000. That’s a $32,000 difference, entirely due to the opportunity cost.

"Zero-cost collars are tactical tools, not strategic hedges; use them for specific, time-bound risks, not perpetual insurance." - Pomegra Learn Library

Conclusion

Zero-cost collars might seem like a free safety net, but they come with strings attached. If your stock surges past the call strike, any gains above that level are off the table. This opportunity cost, combined with friction costs of 1–2% for less-liquid stocks, tax hurdles under IRC §1092, and the risk of early assignment around dividend dates, can add up. As the simulation highlighted, this can translate into tens of thousands of dollars in missed gains over time, making the "zero-cost" label somewhat misleading.

Still, there are situations where this strategy makes sense. Zero-cost collars can work well for concentrated stock positions, executive lock-up periods, or scenarios where selling isn’t an option but downside protection is critical for a defined 1–2 year timeframe. In high-volatility markets, they can even offer surprisingly generous upside caps - sometimes ranging from +68% to +98% above the current price for volatile tech stocks - while providing a firm safety net.

The key takeaway? Use the right tool for the right job. Zero-cost collars are ideal for short-term, cost-conscious protection. Protective puts allow full upside potential while providing a safety cushion. And unhedged stock remains the best choice for long-term growth when liquidity isn’t a concern.

If you’re looking for tailored guidance, advanced tools can help. Platforms like ThetaEdge offer portfolio-aware insights, highlighting protective strategies and multi-leg setups with clear risk and trade-off analysis for every option.

FAQs

What’s the catch with a “zero-cost” collar?

The trade-off lies in the opportunity cost. While you sidestep upfront expenses, you also cap your potential gains. This means you're giving up any upside beyond the cap in return for some level of downside protection. The term "zero-cost" only applies to the lack of an initial payment - it doesn't mean there's no cost involved overall.

How do I choose the put strike and call strike?

To establish a zero-cost collar, start by selecting the put strike (the floor), which determines your level of downside protection. This is typically set around 30% below the stock's current price. Next, set the call strike (the cap) above the current price. The premium received from selling the call is used to offset the cost of purchasing the put. You can fine-tune the collar by adjusting the floor, cap, or expiration date to align with your risk preferences and market expectations.

What tax or assignment risks should I watch for?

If the stock price climbs quickly, you face the risk of early assignment, where the call option might be exercised before its expiration. This would require you to sell your shares, which could lead to realizing capital gains earlier than planned. On top of that, collars can lead to taxable events if the stock is sold at the call strike price. It's essential to weigh these factors carefully when deciding to use this strategy.