How to Calculate Risk for Cash-Secured Puts

Calculate maximum profit, maximum loss and breakeven for cash‑secured puts, and use Delta and Theta to assess assignment risk and time decay.

Compared to covered calls, cash-secured puts are a straightforward options strategy: you sell a put option and set aside enough cash to buy the stock if assigned. The goal? Earn income from the premium while positioning to buy shares at a preferred price. But before jumping in, it’s vital to understand the risks involved.

Here’s what you need to know:

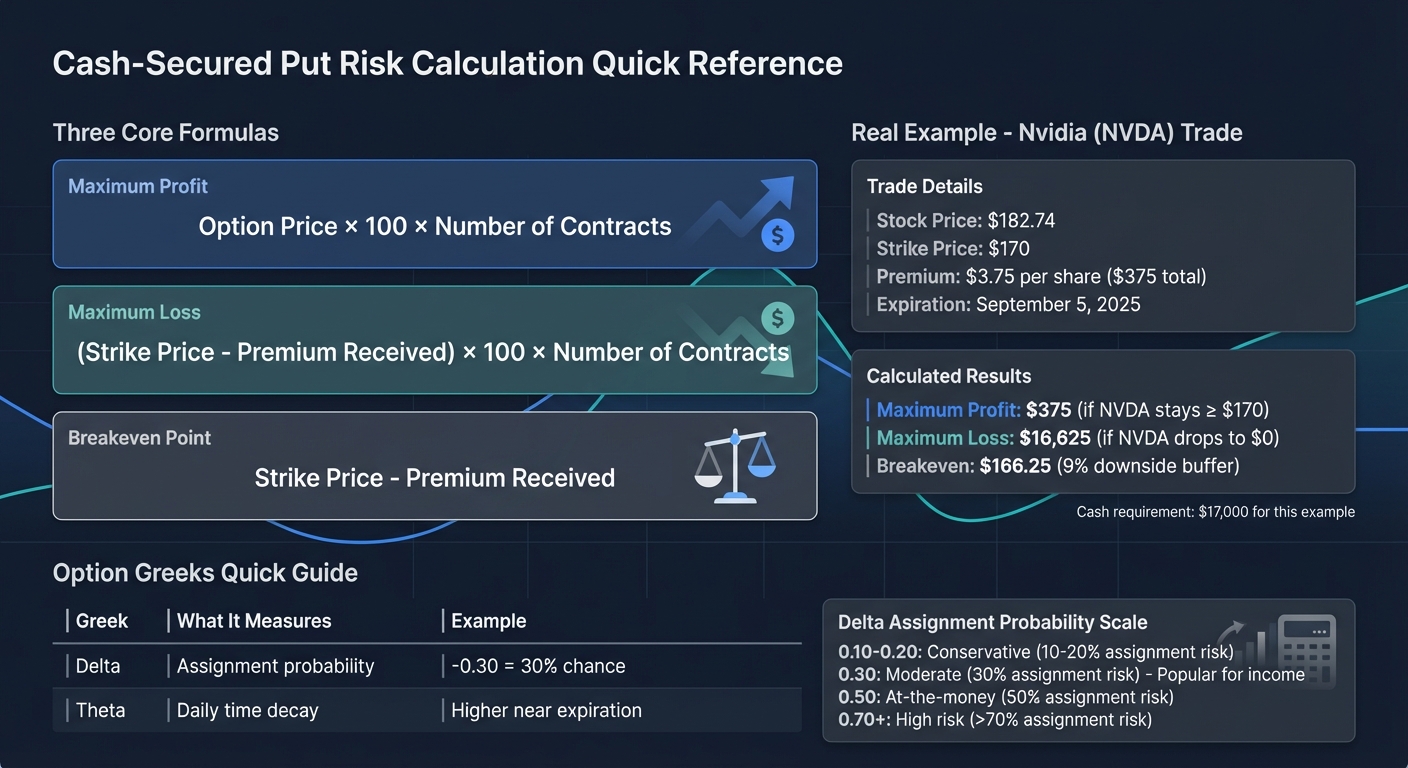

- Maximum Profit: The premium you collect when selling the put. Example: Sell a $170 strike put for $3.75; your max profit is $375 ($3.75 × 100).

-

Maximum Loss: Calculated as

(Strike Price - Premium) × 100. If the stock drops to $0, your loss is significant but offset slightly by the premium. -

Breakeven Point: The stock price where you neither gain nor lose money, calculated as

Strike Price - Premium. Example: $170 strike, $3.75 premium = $166.25 breakeven. - Key Factors: Strike price, volatility, and time to expiration affect risk and reward. Closer strikes and higher volatility mean higher premiums but greater assignment risk.

Use tools like ThetaEdge to simplify these calculations and monitor risks like Delta (assignment probability) and Theta (time decay). Whether you're aiming for income or stock ownership, understanding these metrics ensures smarter decisions with cash-secured puts.

Cash-Secured Put Risk Calculation Formulas and Examples

How to Calculate Maximum Profit

Understanding how to calculate maximum profit is a key part of evaluating the risks and rewards in cash-secured put strategies. For this strategy, the maximum profit is straightforward: it’s the premium you collect when selling the put option. This amount is set once the trade is made and represents the best-case scenario.

What Is the Option Premium?

The premium is the cash payment you receive upfront for agreeing to buy 100 shares at the strike price. This payment is yours to keep, regardless of how the trade unfolds. It serves as compensation for taking on the potential obligation to purchase the stock.

"The maximum profit is achieved when the stock price is at or above the put's strike at expiration because the put will expire worthless. If you sell an option for $777 in premium and it goes to $0, you keep the entire difference."

– Chris Butler, Founder, projectoption

To achieve this maximum profit, the stock price must remain at or above the strike price until the option expires. If this happens, the option becomes worthless, and you retain the full premium.

Example: Maximum Profit Calculation

Let’s look at a specific example. In September 2025, an investor considered a cash-secured put on Nvidia (NVDA) while the stock was trading at $182.74. The investor sold a single $170 strike put option, expiring on September 5, 2025, for a premium of $3.75 per share. Since one options contract represents 100 shares, the total premium collected was $375 ($3.75 × 100). This $375 represents the maximum profit, which would be fully realized if NVDA closed at or above $170 on the expiration date.

The formula for calculating maximum profit is simple:

Option Price × 100 × Number of Contracts

For instance, if you sold two contracts at $3.75 each, your maximum profit would double to $750 ($3.75 × 100 × 2). Be sure to subtract any brokerage fees to determine your net profit.

Up next, we’ll explore how to calculate maximum loss to complete the risk-reward analysis.

sbb-itb-a9ac3c2

How to Calculate Maximum Loss

While the maximum profit in a cash-secured put trade is limited to the premium collected, the potential loss can be much larger. It's crucial to calculate and understand this worst-case scenario before entering a trade.

Maximum Loss Formula

The formula for maximum loss is:

(Strike Price - Premium Received) × 100 × Number of Contracts

This calculation assumes the absolute worst case: the stock's value drops to zero. The premium collected helps offset the loss, making it less severe than simply buying the stock outright at the strike price.

Let’s break this down with an example.

Example: Maximum Loss Calculation

Imagine selling a cash-secured put on Nvidia (NVDA) with a $170 strike price and a $3.75 premium (equivalent to $375 total). If Nvidia's stock price were to plummet to zero, the maximum loss would be $16,625. This is calculated as the $17,000 obligation at the strike price minus the $375 premium received.

To initiate this trade, the investor would need $17,000 in cash held in their account to cover the position. This amount remains locked until the option expires or the position is closed.

"The worst-case scenario (however unlikely) is for the stock price to go to zero, and the investor is assigned 100 shares... That would be like losing $17,000 on the 100 shares of stock, but compensated by the $375 credit initially received."

– Gavin, Blog Author, Options Trading IQ

How Strike Price Selection Affects Risk

The strike price you choose plays a big role in determining your risk. Lower strike prices (further out-of-the-money) reduce both the potential loss and the amount of capital required to secure the trade. However, they also result in smaller premiums.

For instance, data from 2020 to 2025 shows that strike prices 15–20% below the market price carried a 5–10% chance of assignment, while strikes closer to the current price had assignment risks exceeding 70%.

When selecting a strike price, consider whether you'd be comfortable owning the stock at that level. As Doug Ashburn, a Chartered Alternative Investment Analyst, puts it:

"Each time you sell a put option with the intention of eventually acquiring the stock, you're reducing your cost basis... by the amount of premium you collect."

How to Calculate the Breakeven Point

The breakeven point marks the stock price at which your cash-secured put trade transitions from profit to loss. It complements calculations of maximum profit and loss, giving you a fuller picture of the trade's risk and reward.

Breakeven Point Formula

Breakeven = Strike Price - Premium Received

The premium you collect serves as a buffer, effectively lowering your cost basis if you're assigned the shares.

Example: Breakeven Point Calculation

Let’s look at an example from September 2025. Nvidia (NVDA) was trading at $182.74, and an investor sold a $170 strike put, collecting a $3.75 premium per share. The breakeven calculation is straightforward: $170 - $3.75 = $166.25.

This means the stock could fall about 9% - down to $166.25 - before the investor starts losing money, offering a margin of safety.

Here’s another example with Apple (AAPL). When AAPL was trading at $235, a trader sold a $230 strike put for a $4.50 premium. The breakeven point was $225.50 ($230 - $4.50). If assigned, the trader’s effective cost to own the shares would be $225.50 per share.

Knowing your breakeven point helps you decide if you're comfortable with a trade. You can compare it to technical support levels or your ideal entry price for the stock. If the breakeven sits below a strong support level, it provides an added layer of protection.

This calculation is a key step in evaluating risk, setting the stage for more advanced analysis using tools like option Greeks.

Using Option Greeks to Measure Risk

Once you've established your profit and loss boundaries, the next step is to incorporate the option Greeks to get a fuller picture of risk. While knowing your breakeven point is crucial, using metrics like Delta and Theta adds another layer of understanding. These metrics provide insight into how a cash-secured put might behave under changing market conditions, complementing earlier calculations of maximum loss and breakeven.

Delta and Assignment Probability

Delta serves two key purposes: it estimates how much an option's price will change for every $1 move in the underlying stock and provides an approximate probability of assignment. For put options, Delta values range from 0 to -1.0, but traders often ignore the negative sign when assessing assignment probability. For instance, a Delta of -0.30 suggests about a 30% chance of assignment.

"The closer the delta is to zero, the more likely the put will expire worthless, allowing us to keep the premium we collected with no obligation to buy the underlying stock."

– Nasdaq

An at-the-money (ATM) put usually has a Delta near -0.50, reflecting a 50/50 chance of assignment, akin to flipping a coin. Deep in-the-money (ITM) puts, on the other hand, have Deltas approaching -1.0, meaning they move almost dollar-for-dollar with the stock and carry a high likelihood of assignment. Many traders aiming for income prefer selling out-of-the-money (OTM) puts with Deltas between 0.15 and 0.30. This range strikes a balance between collecting a reasonable premium and maintaining a lower risk of assignment.

| Delta Level | Assignment Probability | Risk Profile |

|---|---|---|

| 0.10 to 0.20 | 10% – 20% | Conservative; higher chance of keeping the premium |

| 0.30 | ~30% | Moderate; popular for income strategies |

| 0.50 (ATM) | ~50% | Higher risk; equal chance of assignment or expiration worthless |

| 0.70+ (ITM) | >70% | Very high; assignment is highly likely |

If the Delta of your sold put increases unexpectedly, it signals a greater likelihood of assignment. This might prompt a reassessment of your position. For a deeper dive into your specific holdings, you can use Thetix for AI-powered portfolio analysis to get real-time data and scenario modeling. However, keep in mind that if implied volatility is significantly higher than realized volatility, Delta can overestimate the actual probability of assignment.

Theta and Time Decay

Theta measures how much an option's extrinsic value decreases with each passing day. For sellers of cash-secured puts, this time decay represents the "daily rent" earned as the option's value erodes.

"Theta decay is the only force in the market that helps you automatically every single day."

– Days to Expiry

Time decay isn't uniform. It starts off slow but accelerates as expiration approaches. For example, an option with 90 days to expiration might lose about $0.05 per day, whereas one with only 7 days left could lose $0.40 per day. Interestingly, more than 40% of an option's total profit potential over 45 days is often realized in the final two weeks.

Most traders focus on selling cash-secured puts 30 to 45 days before expiration. This timeframe offers a good balance between premium collection and risk. Positions are often closed or rolled around 21 days to expiration or once 50% to 75% of the maximum potential profit is captured. This approach helps avoid the final week of trading, where sharp price movements (Gamma risk) can quickly erode gains from Theta decay.

Next, we’ll look at how ThetaEdge’s portfolio intelligence simplifies these risk assessments with advanced analytics tools.

Using ThetaEdge for Risk Assessment

Calculating risk for cash-secured puts manually can be a tedious process, involving multiple formulas, spreadsheets, and the interpretation of option Greeks. ThetaEdge simplifies all of this by consolidating the analysis into a single platform. With connections to over 80 brokerages, it provides insights that rival those used by institutional investors, streamlining the process of evaluating key metrics in one place.

Risk Analysis Features in ThetaEdge

ThetaEdge introduces Opportunity Cards, which present critical risk metrics such as breakeven price, maximum loss, profit potential, and assignment probability - all in an easy-to-read format. Additionally, it aggregates option Greeks like Delta, Gamma, Theta, and Vega across your entire portfolio, offering a more comprehensive view of your market exposure rather than isolating individual trades. If a position moves against you, the Roll Opportunities tool offers detailed credit and debit analyses to guide you toward optimal roll strategies.

The platform’s Thetix AI Chat takes risk management a step further by allowing users to ask plain-language questions about specific trades or portfolio risks, eliminating the need for manual calculations. It also generates daily action plans, highlighting expiring positions and suggesting trades to avoid unwanted assignments. This blend of features gives you a clearer and more actionable view of your portfolio.

Example: Evaluating a Cash-Secured Put with ThetaEdge

Imagine selling a cash-secured put on a stock currently trading at $52.00, with a $50 strike price expiring in 35 days, and collecting a $1.20 premium. Instead of manually calculating the breakeven price of $48.80, the maximum loss of $4,880, or the Delta's assignment probability, ThetaEdge’s Opportunity Card instantly provides these details. For example, it might show a Delta of -0.28, indicating a 28% chance of assignment based on historical data and current market conditions.

You could then use Thetix Chat to ask, "How does this $50 put affect my total portfolio Delta?" The AI would deliver a clear breakdown of your overall exposure, helping you decide whether adding this trade increases your downside risk. If the stock were to drop significantly before the option expires, ThetaEdge’s Roll Analysis tool could suggest adjustments, like changing the strike price or extending the expiration date, to improve your risk-reward balance.

"I love how fast ThetaEdge tells me what options to look at. I don't need to dig through a bunch of numbers anymore. It's way less stress trying to figure stuff out alone."

– Robert J., Sales Manager

Summary

Review of Risk Calculation Methods

Let’s recap the key risk metrics discussed earlier. Keep these three formulas in mind:

- Maximum profit: premium × contract size

- Maximum loss: (strike price - premium) × contract size

- Breakeven: strike price - premium per share

Delta serves as a helpful guide for estimating assignment probability (e.g., a Delta of -0.28 suggests a 28% chance of assignment). Theta tracks time decay, which speeds up as expiration nears. Understanding these metrics is crucial for choosing strike prices that match your comfort level as a stockholder.

"Never sell a put strike below a price you'd genuinely like to own the stock at. This keeps you from chasing premium on risky setups." – DaysToExpiry

For those wanting efficiency, automated tools can save time and reduce errors during calculations.

Using ThetaEdge to Simplify Risk Analysis

Crunching these numbers manually can be tedious, especially when comparing multiple strikes and expirations. That’s where ThetaEdge steps in. It streamlines the process by instantly presenting key metrics like breakeven prices, maximum loss, assignment probabilities, and annualized ROI. Instead of juggling spreadsheets or scattered data, you get a clear, consolidated view of how each trade impacts your portfolio.

The Thetix AI Chat makes things even easier. You can ask straightforward questions like, “What’s my total Delta exposure if I add this $50 put?” and get instant answers without doing the math yourself. When market conditions shift, the Roll Opportunities tool provides in-depth recommendations for your next steps. By combining automation with AI-driven insights, ThetaEdge allows you to focus on making informed, confident decisions that align with your risk preferences.

FAQs

What’s the real risk if I’m assigned early?

If you’re assigned early, the primary concern is being obligated to purchase the stock at the strike price. This situation can result in notable losses if the stock's current market value has fallen substantially below the strike price. It's crucial to anticipate and plan for this possibility as part of your broader risk management strategy when using cash-secured puts.

How much cash do I need to reserve per put contract?

To set aside cash for a put contract, take the strike price and multiply it by 100 (since each option contract represents 100 shares). This calculation ensures you have enough funds ready to meet the obligation if the option gets assigned.

When should I roll or close a cash-secured put?

If the stock price dips below the strike price, it might be time to think about rolling or closing a cash-secured put to avoid assignment. Similarly, if the position hits your profit target, or the potential downside risk outweighs any remaining upside, acting promptly can protect your portfolio.

Another key scenario is when the option premium rises sharply, increasing your exposure. Rolling or closing in such cases can help you manage risk effectively. Lastly, freeing up capital for other opportunities is another practical reason to consider adjusting or exiting the trade.