High IV vs Low IV: Best Conditions for Covered Calls

Sell covered calls when IV is high to collect larger premiums; use 0.30–0.40 delta strikes, IV Rank tools, and roll/buyback tactics to manage assignment risk.

When selling covered calls, the level of implied volatility (IV) is a game-changer. Here's the bottom line:

- High IV means higher premiums, offering more income potential. However, it also increases the risk of your shares being called away or facing larger price swings.

- Low IV leads to smaller premiums. While this reduces assignment risk, the income might not justify the effort unless you treat it as a bonus on long-term holdings.

Key insights:

- High IV environments (IV Rank above 70) are ideal for maximizing income, especially during market uncertainty or before major events.

- Low IV environments work best in stable markets but yield less income.

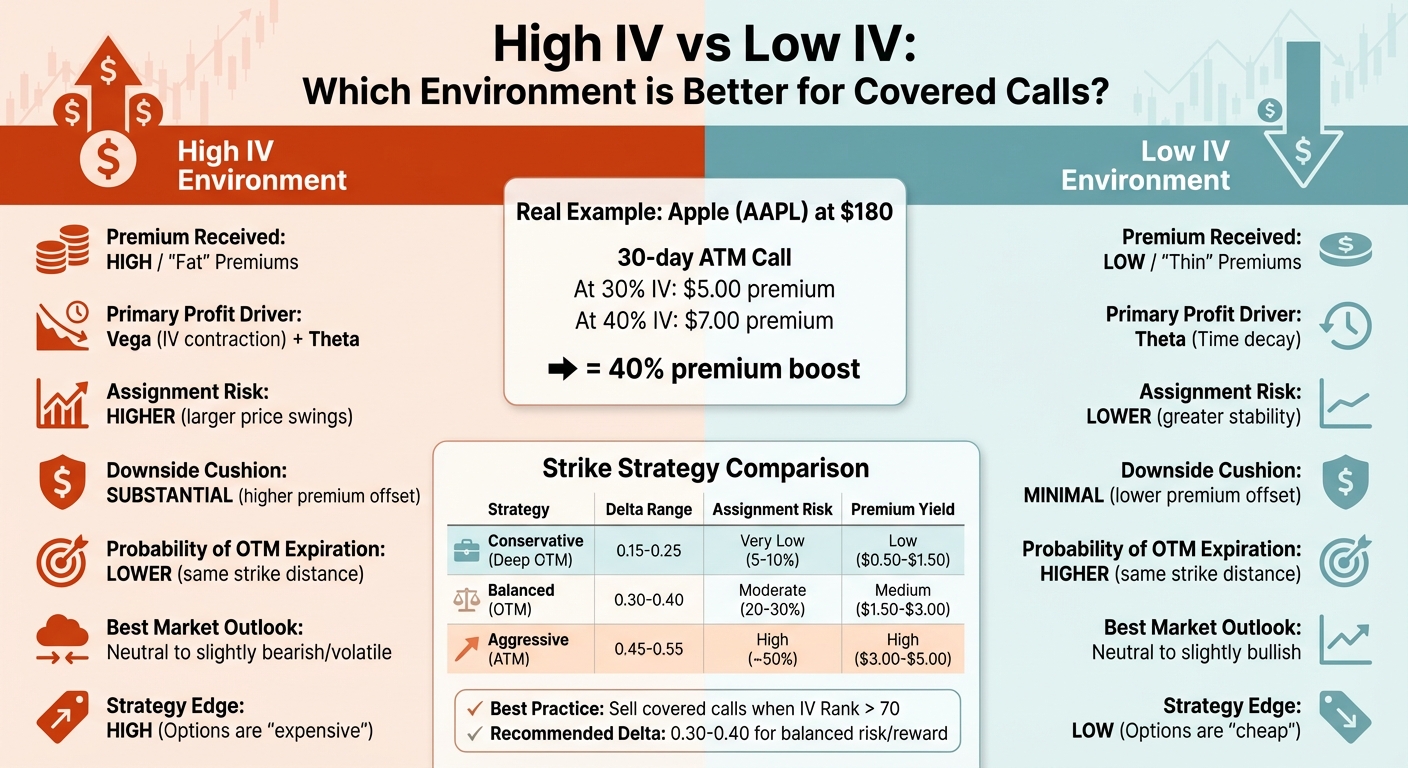

Quick Example: A 30-day at-the-money call on Apple priced at $5.00 with IV at 30% could jump to $7.00 if IV rises to 40%. That’s a 40% boost in premium for the same trade.

The best approach? Sell covered calls when IV is high, focusing on strikes with a 0.30–0.40 delta for a balance between income and assignment risk. Tools like IV Rank and IV Percentile and platforms such as ThetaEdge can help identify the right opportunities and fine-tune your strategy.

Covered Calls in High IV Conditions

Higher Premium Income

When implied volatility (IV) rises, the premiums earned from selling covered calls can increase significantly. This happens because higher IV inflates option prices, making them more expensive.

For example, in November 2025, ApexVol highlighted this with Apple (AAPL) stock trading at $180. A $185 call option with 30 days to expiration was priced at $5.00 when IV was 30%. However, when IV jumped to 40%, the option price increased to $7.00 - a 40% boost in premiums.

"The greater the implied (forecasted) volatility, the richer the option premium." - Alan Ellman, President, The Blue Collar Investor

The best time to sell covered calls is when the IV Rank exceeds 50, and ideally, it should be above 70. At these elevated levels, traders can collect what are often referred to as "fat premiums", providing much higher income opportunities compared to calmer market conditions.

Next, let’s look at how to handle the risks that come with these higher premiums.

Managing Risk in High IV Markets

While high premiums are enticing, they also come with increased risks. Elevated IV indicates the market expects significant price swings, which means your shares are more likely to be called away if the stock price surges past your strike price. On the flip side, a steep drop in the stock price may not be fully offset by the premium collected.

To navigate these risks, consider the following strategies:

- Choose strikes with a 0.30–0.40 delta: This gives you a 60–70% chance the option will expire worthless, allowing you to keep your shares.

- Apply the 50% rule: Once you've captured half of the maximum premium, think about buying back the short call to secure gains and reduce exposure to further volatility.

- Roll up and out: If the stock nears your strike price, you can buy back the current call and sell a higher-strike call with a later expiration. This lets you stay in the trade while earning additional premium.

Each of these approaches can help balance the potential rewards with the risks of high IV conditions.

High IV Metrics Table

| Strike Strategy | Delta (Assignment Probability) | Premium Yield | Assignment Risk | Breakeven Price |

|---|---|---|---|---|

| Conservative (Deep OTM) | 0.15 – 0.25 | Low ($0.50 – $1.50) | Very Low (5–10%) | Stock Price - Low Premium |

| Balanced (OTM) | 0.25 – 0.40 | Medium ($1.50 – $3.00) | Moderate (20–30%) | Stock Price - Medium Premium |

| Aggressive (ATM) | 0.45 – 0.55 | High ($3.00 – $5.00) | High (~50%) | Stock Price - High Premium |

Premium examples are based on stock prices ranging from $100 to $200.

Covered Calls in Low IV Conditions

Lower Premium Income

When implied volatility (IV) is low, the premiums from selling covered calls take a noticeable hit. This happens because low IV signals smaller expected price movements, which reduces the extrinsic value of options.

"When volatility is low, option premiums shrink. Even if the stock's price stays strong, even strong stock prices yield notably lower premiums." – REX Shares

Take Tesla as an example: a 30-day at-the-money (ATM) call generates about a 7% annualized return when IV is at 25%, but jumps to 21% when IV rises to 55%. In quieter market conditions, the trade-off is evident - reduced assignment risk but also much smaller premiums.

That said, this strategy can still work in low IV environments if you treat the premium as a bonus on top of your long-term holdings rather than a primary income source. However, avoid the temptation to chase higher yields by selling calls too close to the current stock price. The slight increase in premium is rarely worth the risk of losing shares you want to keep.

Managing Risk in Low IV Markets

One upside of low IV is a reduced chance of assignment. With calmer price expectations, the likelihood of your stock surging past the strike price is significantly lower. For example, from 1986 to 2023, the Cboe S&P 500 BuyWrite Index experienced about 30% less volatility than the S&P 500, with its worst decline at 35.8% compared to a 51% drop for the broader index.

But here’s the downside: lower premiums provide limited downside protection and cap your potential gains during strong market rallies.

To make the most of these conditions, consider selling calls with deltas in the 0.30 to 0.40 range. This typically offers a 60–70% chance of the options expiring worthless. Additionally, it’s wise to wait for events like earnings announcements - periods often marked by higher volatility - before selling calls, as this can help you avoid locking in underwhelming premiums.

Below is a breakdown of strike selection strategies tailored for low IV markets.

Low IV Metrics Table

| Strike Strategy | Recommended Delta Range | Premium Yield | Assignment Risk | Breakeven Consideration |

|---|---|---|---|---|

| Conservative (Deep OTM) | Lower than moderate | Very low | Minimal | Stock price reduced by only a small premium |

| Balanced (OTM) | Approximately 0.30–0.40 | Modest | Lower | Stock price offset by a modest premium |

| Aggressive (ATM) | Approaching at-the-money | Relatively higher | Increased | Stock price reduced by a moderate premium |

These metrics reflect common patterns observed in low IV scenarios.

High IV vs Low IV: Direct Comparison

High IV vs Low IV Covered Calls Comparison Chart

Key Metrics Comparison Table

When comparing high and low implied volatility (IV) environments, the numbers tell a clear story. Here's a side-by-side breakdown of the key metrics:

| Metric | High IV Environment | Low IV Environment |

|---|---|---|

| Premium Received | High / "Fat" Premiums | Low / "Thin" Premiums |

| Primary Profit Driver | Vega (IV contraction) and Theta | Theta (Time decay) |

| Assignment Risk | Higher (due to larger price swings) | Lower (due to greater stability) |

| Downside Cushion | Substantial (higher premium offset) | Minimal (lower premium offset) |

| Probability of OTM Expiration | Lower (for the same strike distance) | Higher (for the same strike distance) |

| Best Market Outlook | Neutral to slightly bearish/volatile | Neutral to slightly bullish |

| Strategy Edge | High (Options are "expensive") | Low (Options are "cheap") |

This comparison highlights the trade-offs between the two environments. For example, imagine a 30-day at-the-money call on Apple (AAPL) priced at $180. If IV is at 30%, the premium might be $5.00. But if IV rises to 40%, the premium could jump to $7.00 - a 40% boost in income for the same position.

Pros and Cons of Each IV Environment

High IV environments offer bigger premiums, which can help offset downside moves. However, they come with increased assignment risk due to larger price swings. On the flip side, sellers benefit from Vega contraction as uncertainty fades.

"Higher IV = More Expensive Options... Sell options when IV is HIGH (collect fat premiums, profit from Vega contraction)." – ApexVol Trading Team

In contrast, low IV environments are much calmer. Assignment risk is lower, but premiums are often too small to provide meaningful protection. This thinner cushion also limits potential gains during rallies.

Historical data backs up these insights. From 1986 to 2023, the Cboe S&P 500 BuyWrite Index achieved annualized returns of 8.2%, compared to 10.5% for the S&P 500. While the BuyWrite Index captured about 61% of the S&P 500's gains during bull markets (due to its upside cap), it experienced 30% less volatility and a maximum drawdown of 35.8%, compared to the broader index's 51%.

sbb-itb-a9ac3c2

Best Conditions and Using ThetaEdge for IV Analysis

When to Use Covered Calls Based on IV

The best time to use covered calls is when you're dealing with neutral to slightly bullish stocks that have high implied volatility (IV). A good rule of thumb is to look for an IV Rank or IV Percentile above 70. This combination allows you to collect higher premiums without taking on extra risk with the underlying stock. Covered calls are most effective after a strong upward move when the stock's momentum starts to slow down. At this point, elevated IV and faster time decay and time-based exits work to your advantage.

However, it's important to steer clear of chasing high premiums on stocks with weak fundamentals or those labeled as "meme" stocks. These can carry a higher risk of assignment, which could derail your strategy. This is where tools like ThetaEdge can fine-tune your approach to IV analysis, helping you pinpoint the best entry points.

How ThetaEdge Helps with IV Analysis

ThetaEdge takes the guesswork out of IV analysis by offering tools designed to spot and act on covered call opportunities. Its IV Rank and IV Percentile metrics compare a stock’s current volatility to its 52-week range. This helps you determine whether options are priced higher or lower than usual. The RT Spread Scanner goes a step further by ranking stock and short call combinations based on their risk and reward potential.

To balance income potential with covered call risk management, ThetaEdge provides assignment probability calculations. It also features the Thetix AI assistant, which delivers actionable insights by analyzing your portfolio. PnL calculators let you see how premiums can offset losses or cap gains. Smart alerts are another key feature, notifying you when upside momentum stretches too far or when IV hits specific thresholds, like those often seen before earnings announcements. During the beta phase, these advanced tools are free to use, giving you access to professional-grade analytics for maximizing income while managing risks effectively.

Conclusion

Implied volatility (IV) plays a central role in driving the success of any covered call strategy. When IV is high - typically with an IV Rank above 70 - you can collect higher premiums, which help offset downside risks and generate solid income. On the flip side, low IV environments result in smaller premiums, making the strategy less appealing. The key is to sell into strength: wait for volatility spikes, then deploy your covered calls to take advantage of higher premiums and potential IV contraction. This timing can significantly improve your outcomes.

Understanding the context is essential. Tools like IV Rank and IV Percentile help determine whether current volatility is high or low compared to a stock's 52-week history. Platforms like ThetaEdge enhance this process by using real-time IV metrics, assignment probabilities, and Thetix AI insights to identify the best entry points.

The most effective covered call strategies thrive in neutral to moderately bullish markets paired with elevated IV levels. As Warren Buffett famously said, "Be fearful when others are greedy, and greedy when others are fearful". This mindset aligns perfectly with selling options, especially when market fear pushes premiums higher.

Advanced trading tools can elevate these strategies even further. During its beta phase, ThetaEdge offers free access to institutional-grade analytics, including tools to calculate Greeks, track income, and manage risk. In any market condition, having access to precise data can help you optimize income while keeping risks under control.

FAQs

What are the risks of selling covered calls when implied volatility is high?

Selling covered calls during periods of high implied volatility (IV) can be a double-edged sword. On one hand, high IV means higher premiums for the calls you sell, which can be appealing. But on the other hand, it comes with heightened risks because larger price swings are more likely.

When IV is high, the market expects bigger price movements. If the stock price rises sharply above the strike price, your shares might be called away at that level, limiting how much you can gain. At the same time, a steep drop in the stock price could lead to losses. While the premium you collect from selling the call provides some buffer, it might not fully offset the drop.

High IV often shows up during uncertain times or around events like earnings reports, where sudden price gaps are common. These unpredictable shifts can mean selling your shares under less-than-ideal conditions or facing losses that exceed expectations. While the higher premiums can be tempting, navigating high IV environments requires careful timing and a solid risk management plan to weigh the potential rewards against the risks.

When is the best time to sell covered calls based on implied volatility?

The ideal time to sell covered calls is when implied volatility (IV) is elevated. Why? Because higher IV indicates the market is anticipating larger price swings, which drives up option premiums. By selling covered calls during these periods, you can secure higher premiums, which enhances your income potential.

Periods of high IV often occur before major market events, such as earnings announcements. However, after these events, IV usually drops - a phenomenon known as "IV crush." Keeping an eye on IV levels, like IV rank or IV percentile, can help you spot when IV is high relative to its historical range, signaling a prime opportunity to sell.

In contrast, selling covered calls during low IV conditions typically results in smaller premiums, limiting your income potential. By targeting times of elevated IV, you can make the most of your covered call strategy and better align it with your income-focused goals.

How can I manage assignment risk when using covered calls in different IV conditions?

Managing assignment risk with covered calls means tailoring your approach to match the current implied volatility (IV) levels.

In high IV markets, options premiums tend to be higher, which can boost your income potential. However, this also comes with an increased chance of your shares being called away due to larger expected price swings. To manage this, you might sell calls with strike prices further out-of-the-money. This reduces the likelihood of assignment while still allowing you to collect a premium. If the stock price moves unexpectedly, rolling your calls - buying back the existing contract and opening a new one with a different strike price or expiration - can help you regain control of your position.

In low IV markets, premiums are smaller, reflecting the reduced likelihood of significant price moves. While this lowers your income potential, the risk of assignment is also lower. In such conditions, selling calls at strike prices that align with modest profit goals can be a smart move. To further protect yourself, you could combine your covered call with a protective put, creating a collar strategy. This approach limits your downside risk while still allowing for some income generation.

By adjusting your strike prices and incorporating protective strategies, you can navigate assignment risk effectively, no matter how the market behaves.