Intrinsic vs Extrinsic Value: Covered Call Insights

Clear breakdown of intrinsic vs extrinsic option value and how time decay, strike choice, and volatility shape covered call income and assignment risk.

When selling covered calls, the option premium you collect has two parts: intrinsic value and extrinsic value. Understanding these components helps you make better decisions about strike prices, expiration dates, and covered call risk management.

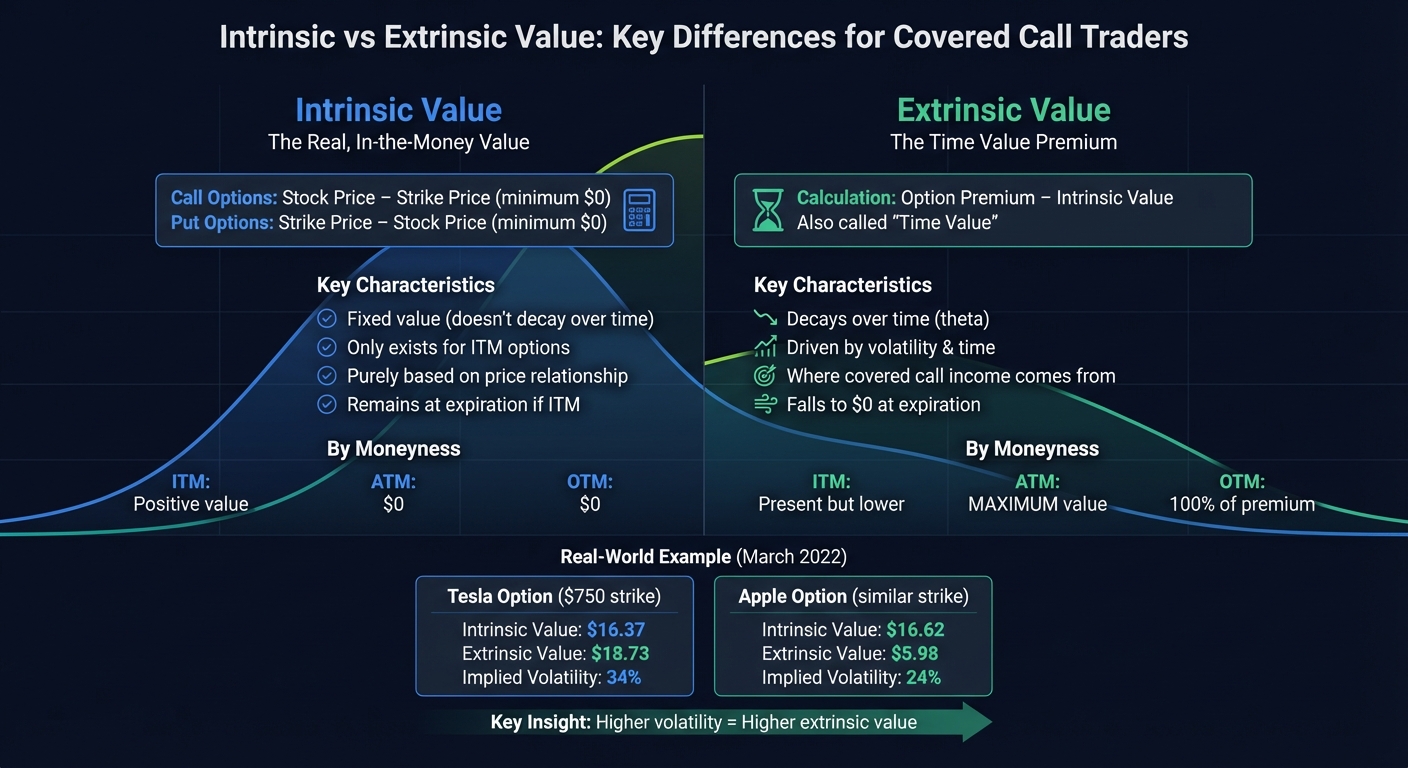

- Intrinsic Value: The immediate profit if the option is exercised now. For call options, it's the stock price minus the strike price (if positive).

- Extrinsic Value: The "time value" of the option, driven by time until expiration, market volatility, and other factors. This is where most of your income as a covered call seller comes from.

Key points to know:

- Intrinsic value is fixed and only exists for in-the-money (ITM) options.

- Extrinsic value decreases over time due to time decay (theta), accelerating as expiration nears.

- At-the-money (ATM) options have the highest extrinsic value, while out-of-the-money (OTM) options are entirely extrinsic.

Strike price selection is critical:

- ITM strikes offer downside protection but limit upside potential and increase early assignment risk.

- ATM strikes maximize extrinsic value but provide no intrinsic buffer.

- OTM strikes allow for potential stock price gains but provide lower premiums upfront.

What is Intrinsic Value?

Intrinsic value represents the profit you’d gain if you exercised an option immediately. It’s a straightforward calculation: for call options, it’s the difference between the stock price and the strike price, but only if the stock price is higher. For instance, if a stock is trading at $55 and the strike price is $50, the intrinsic value is $5. If the stock price is below the strike, the intrinsic value is zero.

"Intrinsic value is the real, in-the-money value of an option. In other words, it's the financial payout if you immediately exercised the option." - Jonathan Hobbs, CFA, IncomeShares

This value doesn’t depend on time or volatility - it’s purely a reflection of how the stock price compares to the strike price. By the time an option reaches expiration, its premium is entirely made up of intrinsic value, as any extrinsic value will have disappeared.

For those comparing covered calls vs cash-secured puts, understanding intrinsic value is key to evaluating the risk of assignment. When a call option has high intrinsic value and minimal extrinsic value, the likelihood of early exercise increases, especially around ex-dividend dates. Additionally, brokers will automatically exercise options at expiration if they’re in-the-money by at least $0.01. Knowing this helps you anticipate when a covered call might be exercised and prepares you for the next step: analyzing extrinsic value and its role in your strategy.

sbb-itb-a9ac3c2

What is Extrinsic Value?

Extrinsic value represents the portion of an option's premium that goes beyond its immediate profit potential. It reflects the uncertainties tied to time and market volatility, often referred to as time value.

"Think of extrinsic value as the insurance premium paid for future opportunity." - MoneyPulses Team

The amount of extrinsic value in an option is influenced by two key factors: time until expiration and implied volatility. Options with more time left before they expire have higher extrinsic value because there’s a greater chance for the underlying asset’s price to move in a favorable direction. Similarly, options tied to assets with higher implied volatility - indicating larger anticipated price swings - carry more extrinsic value. For instance, a stock with an implied volatility (IV) of 70% will have options with higher extrinsic value compared to one with an IV of 30%. While interest rates and dividend yields also play a role, their effects are generally smaller.

For those selling covered calls, extrinsic value is where the income comes from. When you sell a call option against shares you own, you collect this "time-based premium" upfront. Ideally, the option expires worthless or out-of-the-money (OTM), letting you keep the full premium as profit. OTM options are made up entirely of extrinsic value, while at-the-money (ATM) options generally have the highest extrinsic value because they are most sensitive to changes in time and volatility.

It's important to note that extrinsic value doesn't diminish evenly over time. Roughly one-third of an option's extrinsic value decays in the first half of its life, while the remaining two-thirds erodes in the second half. This uneven decay, known as theta, accelerates as expiration approaches, especially in the final 30 to 45 days. For covered call sellers, this works to your advantage - by collecting the premium upfront, you benefit as the option’s value erodes more rapidly near expiration. By the time the option expires, its extrinsic value drops to zero, leaving only intrinsic value.

Timing is everything when it comes to selling covered calls. To maximize income, aim to sell when implied volatility is high and choose expiration dates where time decay is most pronounced. This understanding of extrinsic value and its decay is essential for selecting the right strike prices and optimizing your covered call strategy.

Key Differences Between Intrinsic and Extrinsic Value

Intrinsic vs Extrinsic Value in Options Trading: Key Differences

Let’s dive deeper into what sets intrinsic value apart from extrinsic value, focusing on how they operate and what drives their behavior.

Intrinsic value represents the immediate profit you’d gain if you exercised the option right now. It’s calculated as the difference between the stock price and the strike price, but if this difference is negative, the intrinsic value is simply $0.

"Intrinsic value answers one simple question: If I exercised this option right now, would I make money?" - MoneyPulses Team

Extrinsic value, on the other hand, is the portion of the option premium that exceeds its intrinsic value. It reflects the option’s potential future profitability and is influenced by factors like time until expiration, implied volatility, interest rates, and dividends. Unlike intrinsic value, which depends purely on the price relationship between the stock and the strike, extrinsic value is dynamic and erodes over time due to theta decay.

For instance, in March 2022, a Tesla option with a $750 strike had an intrinsic value of $16.37 and an extrinsic value of $18.73. In contrast, an Apple option with a similar intrinsic value of $16.62 had only $5.98 in extrinsic value. The difference stemmed from Tesla’s implied volatility being 34%, compared to Apple’s 24%. This illustrates how volatility significantly impacts extrinsic value.

Comparison Table: Intrinsic vs Extrinsic Value

| Feature | Intrinsic Value | Extrinsic Value |

|---|---|---|

| Calculation (Call) | Stock Price − Strike Price (minimum $0) | Option Premium − Intrinsic Value |

| Calculation (Put) | Strike Price − Stock Price (minimum $0) | Option Premium − Intrinsic Value |

| Primary Drivers | Underlying price relative to the strike price | Time to expiration, volatility, interest rates |

| Time Decay Impact | None - remains constant if price relationship holds | Erodes daily, faster as expiration nears |

| In-the-Money (ITM) | Positive value exists | Present but relatively lower |

| At-the-Money (ATM) | Zero | Maximum extrinsic value |

| Out-of-the-Money (OTM) | Zero | Makes up 100% of the option’s premium |

| Value at Expiration | Exists if ITM | Falls to $0 |

Grasping these differences is critical when choosing ITM vs. OTM strike prices and planning effective covered call strategies.

How to Apply Intrinsic and Extrinsic Value in Covered Calls

Let’s take the concepts of intrinsic and extrinsic value and put them to work in the world of covered calls. These two components play a crucial role in shaping your strategy, influencing the balance between income, downside protection, and the potential for gains in your covered call strategy.

The strike price you select dictates how much of your premium comes from intrinsic versus extrinsic value. This choice isn’t just about numbers - it’s about aligning your strategy with your market outlook and investment goals.

Market outlook drives strike selection. If you’re optimistic about a stock’s potential, out-of-the-money (OTM) strikes are the way to go. These consist entirely of extrinsic value, allowing you to benefit from time decay while leaving room for share price appreciation. On the other hand, if you’re looking for downside protection, in-the-money (ITM) strikes provide a cushion through their intrinsic value. However, this comes at the cost of limiting upside potential and increases the chance of early assignment.

"I use ATM and OTM strikes when I am bullish about the stock and overall market conditions. I favor ITM strikes when I'm bearish about the overall market or when the technicals of the stock are mixed." - Alan Ellman, President, The Blue Collar Investor

For income-focused strategies, at-the-money (ATM) strikes are key. These options maximize extrinsic value since they lack intrinsic value entirely. Their rapid time decay makes them ideal for neutral market conditions, although they don’t leave room for additional capital gains.

Selecting Strike Prices Using Intrinsic and Extrinsic Value

Choosing the right strike price is about more than just boosting premium income - it’s also about managing risk effectively. This balance is central to a strong covered call strategy.

The premium’s breakdown between intrinsic and extrinsic value should match your objectives. Extrinsic value rewards you for time decay, while intrinsic value reflects immediate, in-the-money profit.

Consider this example from May 2012 with Ascena Retail Group (ASNA), trading near $21:

- An ITM $20 strike offered a 3.5% return with 4.1% downside protection, thanks to its intrinsic value cushion.

- An ATM $21 strike delivered the highest return at 4.6% but provided no downside buffer or room for capital gains.

- An OTM $22 strike yielded a 2.6% return upfront, with 5.5% upside potential - totaling a possible 8.1% return over five weeks if the stock appreciated.

Monitor extrinsic value as an exit signal. When extrinsic value dwindles to negligible levels - around $0.05 to $0.15 - there’s little left to gain, and the risk of early assignment grows, particularly for ITM options. Tyler Craig from Tackle Trading explains:

"When the extrinsic value runs to zero, you can't make any more profit due to time decay. Thus, you should exit or adjust the trade to keep the dream alive." - Tyler Craig, CMT, Tackle Trading

To strike a balance between premium collection and flexibility, experienced sellers often target options with around 45 days to expiration. This timeframe captures significant extrinsic value while avoiding the slower decay of longer-term contracts.

Example Table: Covered Call Scenarios

Here’s a breakdown of how different strike prices affect intrinsic and extrinsic value for a stock trading at $37.00. This table highlights how each choice impacts income and upside potential.

| Strike Price | Moneyness | Call Bid | Intrinsic Value | Extrinsic Value | Upside Potential |

|---|---|---|---|---|---|

| $30.00 | ITM | $9.40 | $7.00 | $2.40 | $0.00 |

| $35.00 | ITM | $5.20 | $2.00 | $3.20 | $0.00 |

| $40.00 | OTM | $1.90 | $0.00 | $1.90 | $3.00 |

| $45.00 | OTM | $0.80 | $0.00 | $0.80 | $8.00 |

Note: Upside Potential refers to the additional profit if the stock price rises to the strike price.

Time Decay and Its Impact on Extrinsic Value

Time decay, or theta, plays a central role in options trading. It represents how an option's extrinsic value diminishes each day as expiration nears. This decline isn’t linear - it speeds up significantly in the final weeks, which is especially relevant for covered call writers.

Interestingly, an option sheds about one-third of its time value during the first half of its lifespan, while the remaining two-thirds vanish in the second half. Early in the contract, the decay might be modest, around $0.08 per day, but as expiration approaches, it can jump to roughly $0.30 per day during the final week.

For covered call writers, this creates an ideal timeframe often referred to as the "Goldilocks zone" - the sweet spot of 30 to 45 days before expiration. During this period, theta accelerates enough to provide attractive premium income without exposing the position to the heightened price sensitivity of the final days. In fact, over 70% of an option's theta-based profit is typically achieved within the last three weeks.

However, as expiration nears, gamma - which measures how sensitive an option’s price is to small changes in the underlying stock - becomes a bigger factor. In the final week, gamma can spike dramatically, meaning even a slight unfavorable stock movement could erase weeks of theta gains.

"Theta is what you earn from time decay. Gamma is the cost when the stock moves against you." - Days to Expiry

This delicate balance between theta and gamma highlights the need for vigilance in managing covered call positions. Many seasoned traders adhere to the 21-day rule, closing or rolling their positions when 21 days are left. By this point, they’ve often secured 60% to 80% of the maximum profit while sidestepping the high-risk "binary zone" of the final days. Understanding these dynamics is essential for fine-tuning your strategy and deciding when to exit or adjust your positions.

How ThetaEdge Enhances Covered Call Strategies

ThetaEdge focuses on time decay to help investors make the most of extrinsic value in their covered call strategies. Success in managing covered calls hinges on understanding the difference between intrinsic and extrinsic value - from choosing strike prices to deciding when to close or roll positions. ThetaEdge simplifies this process, offering tools that isolate extrinsic value, which is the actual profit driver in covered calls. This targeted approach lays the foundation for the platform’s advanced, AI-powered features.

The platform calculates your potential profit by zeroing in on extrinsic value. For in-the-money calls, it automatically removes the intrinsic portion (Stock Price − Strike Price) from the total premium, showing the actual income you can earn from time decay. This prevents the common error of overestimating returns by including intrinsic value, which would be forfeited if the position is assigned.

AI tools also refine timing decisions. ThetaEdge tracks theta to pinpoint optimal periods for selling calls, often around 45 days before expiration when time decay accelerates. Additionally, it monitors implied volatility (IV), alerting you to periods of elevated IV that offer higher premiums or warning of a potential "volatility crush" after events like earnings announcements.

Key Features for Value and Risk Analysis

ThetaEdge goes beyond calculations with specialized tools for deeper insights. The platform’s Thetix AI assistant delivers tailored, portfolio-specific advice. Instead of relying on manual calculations, you’ll receive clear risk/reward metrics and assignment probabilities for every covered call opportunity, helping you maximize income.

The income tracking dashboard focuses on extrinsic value captured rather than just premiums collected, offering a more accurate measure of performance. Combined with portfolio Greeks for overall risk analysis and daily AI-generated action plans, you gain a full view of how factors like time decay, volatility shifts, and price changes affect your positions. With integration across 80+ brokerages, ThetaEdge allows you to evaluate opportunities from all your accounts in one place.

Conclusion

Understanding the distinction between intrinsic and extrinsic value is key to refining your covered call strategy. Intrinsic value represents immediate profit, while extrinsic value - driven by time decay - forms the basis for generating income through covered calls.

To achieve consistent income, focus on the extrinsic value component. Remember, when you sell an in-the-money call, only the extrinsic portion of the premium contributes to potential profit as time passes. As discussed earlier, choosing the right strike price and timing your trades carefully are critical to balancing income potential with risk.

ThetaEdge streamlines this process by automatically breaking down intrinsic and extrinsic value, giving you a clear picture of the income potential in your trades. With AI-driven timing insights, detailed metrics, and portfolio-wide analysis, you can confidently target extrinsic value to enhance your covered call returns and boost portfolio income efficiently.

FAQs

How do I quickly separate intrinsic and extrinsic value in a call premium?

To break down a call premium into intrinsic value and extrinsic value, start by calculating the intrinsic value. This is the difference between the stock price and the strike price, but only if the option is in-the-money. For instance, if the stock is trading at $100 and the strike price is $90, the intrinsic value is $10.

Next, subtract the intrinsic value from the total premium. The remaining amount is the extrinsic value, which accounts for factors like time until expiration and market volatility.

When should I close or roll a covered call to avoid early assignment?

When managing a covered call, it’s worth thinking about closing or rolling the position under specific conditions. Two key signals to watch for are when the option’s delta increases to around 0.55–0.65 or when the time value falls below 10–15% of the option’s total price. These changes suggest a greater chance of early assignment, especially if the stock’s price climbs or the extrinsic value of the option drops sharply.

Rolling a covered call means closing your existing position and opening a new one. This approach helps you adjust for changing market conditions while continuing to manage risk and generate income.

What expiration range best balances theta decay and price-move risk?

An expiration period of roughly 30 days often strikes a good balance between theta decay and price movement risk. This timeframe provides a reasonable window for managing your position, avoiding the rapid adjustments often required with shorter expirations, while also limiting the extended exposure tied to longer durations. It lets you take advantage of consistent theta decay without needing to tweak your strategy too often.